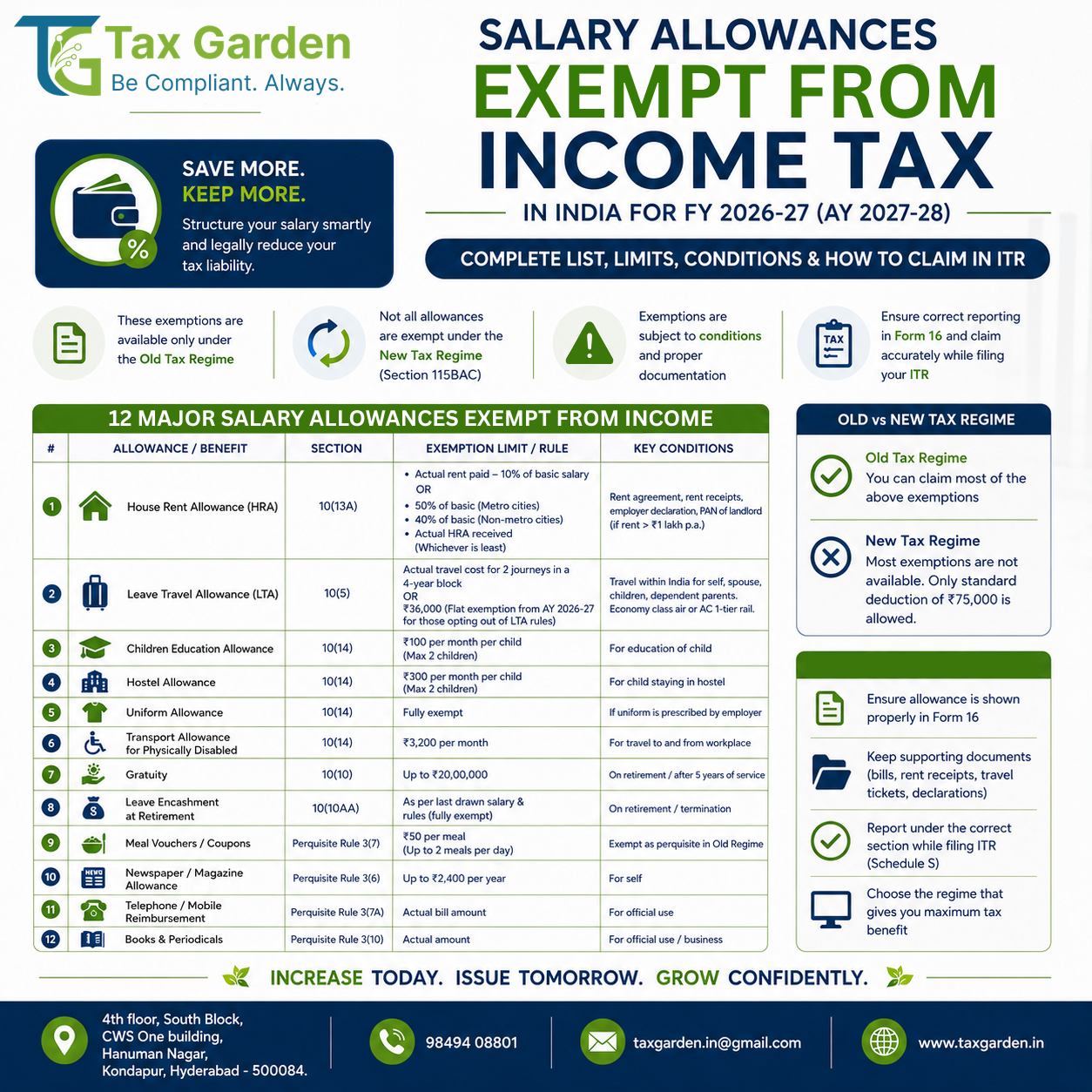

Key Takeaways

- Most salary allowance exemptions (HRA under Section 10(13A), LTA under Section 10(5), and the Section 10(14) special allowances) are available only under the old tax regime. The new regime under Section 115BAC is now the default, so you forfeit these unless you opt out.

- A handful of exemptions survive in both regimes: transport allowance for disabled employees (Rs 3,200/month), conveyance and travel allowances incurred for official duty, and the statutory retirement exemptions for gratuity, leave encashment, and commuted pension.

- HRA exemption is the least of three figures, and the 50% rate applies only in four metro cities: Delhi, Mumbai, Kolkata, and Chennai. Every other city, including Bengaluru, Hyderabad, Pune, and Gurugram, is treated as non-metro at 40%.

- Gratuity is exempt up to Rs 20 lakh and leave encashment up to Rs 25 lakh for non-government employees, both across your working life, not per employer.

- The old regime rewards employees with high rent, LTA, and structured allowances. The new regime rewards those with few exemptions and a higher standard deduction. Run both before you choose.

Which salary allowances are exempt from income tax in FY 2026-27? HRA, LTA, children education and hostel allowances, uniform and conveyance allowances, transport allowance for disabled employees, gratuity, leave encashment, and commuted pension. Most Section 10(14) and HRA/LTA exemptions apply only in the old regime; retirement and disability allowances apply in both. (Source: Sections 10(5), 10(10), 10(10AA), 10(13A), 10(14), incometaxindia.gov.in)

Your CTC and your taxable salary are rarely the same number. A well-structured salary carves out components that the Income Tax Act, 1961 exempts either fully or up to a statutory ceiling. Those exemptions are the difference between paying tax on your entire package and paying tax only on what is genuinely income in your hands.

The catch in FY 2026-27 is that the new tax regime under Section 115BAC is the default. It strips away almost every allowance exemption in exchange for wider slabs and a larger standard deduction. So the question is no longer only "which allowances are exempt," but "which allowances are exempt under the regime I have chosen." This guide covers both.

Looking for expert help with salary allowances exempt from income tax India? The team at Tax Garden, based in Kondapur, Hyderabad, helps Indian SMEs stay compliant end-to-end: filings, notices, and advisory, all in one place.

The Complete List of Exempt Salary Allowances

The table below is the quick reference. Each figure is a statutory limit, and each allowance carries conditions that we unpack in the sections that follow. "Both" in the regime column means the exemption survives even if you stay on the default new regime.

| Allowance | Section | Exemption Limit | Regime |

|---|---|---|---|

| House Rent Allowance (HRA) | 10(13A) | Least of: actual HRA, rent paid minus 10% of salary, or 50% (metro) / 40% (non-metro) of salary | Old only |

| Leave Travel Allowance (LTA) | 10(5) | Actual economy-air or AC-first-class rail fare; 2 journeys per 4-year block | Old only |

| Children Education Allowance | 10(14) | Rs 100 per month per child, up to 2 children | Old only |

| Hostel Expenditure Allowance | 10(14) | Rs 300 per month per child, up to 2 children | Old only |

| Uniform Allowance | 10(14) | Actual amount spent on purchase/upkeep of prescribed uniform | Both |

| Transport Allowance (disabled) | 10(14) | Rs 3,200 per month | Both |

| Conveyance Allowance (duty) | 10(14) | Actual expenditure incurred on official duty | Both |

| Travel / Daily Allowance (tour, transfer) | 10(14) | Actual expenditure on tour or transfer | Both |

| Gratuity (non-government) | 10(10) | Up to Rs 20 lakh (lifetime) | Both |

| Leave Encashment (non-government) | 10(10AA) | Up to Rs 25 lakh (lifetime) | Both |

| Commuted Pension | 10(10A) | 1/3 (with gratuity) or 1/2 (without) of pension | Both |

| Meal / Food Coupons | Rule 3(7)(iii) | Rs 50 per meal, up to 2 meals per working day | Old only |

House Rent Allowance: Section 10(13A)

HRA is the largest exemption for most salaried tenants. Under Section 10(13A) read with Rule 2A, the exempt amount is the least of three figures:

- The actual HRA received from your employer

- Rent actually paid minus 10% of salary

- 50% of salary if you live in a metro city, or 40% if you live anywhere else

"Salary" here means basic salary plus dearness allowance (if it forms part of retirement benefits) plus any commission based on a fixed percentage of turnover. It is not your gross CTC.

The metro question causes the most confusion. For HRA purposes, only four cities qualify for the 50% rate: Delhi, Mumbai, Kolkata, and Chennai. Despite their size and cost of living, Bengaluru, Hyderabad, Pune, Gurugram, Noida, and every other city are treated as non-metro and capped at 40%. Proposals to widen this list circulate regularly, but Rule 2A has not been amended, so apply the four-city rule.

HRA exemption is available only in the old regime. If you opt for or default into the new regime, your entire HRA is taxable regardless of how much rent you pay. For the full mechanics, worked examples, and documentation rules, see our detailed HRA exemption guide under Section 10(13A).

Tax Rate Chart

HRA: 50% Metro vs 40% Non-Metro

The third cap in the HRA formula depends only on your city

Metro (Delhi, Mumbai, Kolkata, Chennai)

Cap of 50% of salary

All other cities (non-metro)

Includes Bengaluru, Hyderabad, Pune, Gurugram

Source: Section 10(13A), Rule 2A, Income Tax Act; incometaxindia.gov.in

Leave Travel Allowance: Section 10(5)

LTA exempts the travel cost of a holiday within India, subject to tight conditions under Section 10(5) read with Rule 2B:

- The exemption covers actual travel cost only, not hotels, food, or local sightseeing.

- Travel must be domestic. Any foreign leg is fully taxable.

- The exempt fare is capped at economy-class air fare by the shortest route, or AC first-class rail fare where the journey is by rail or a mode other than air.

- You may claim exemption for two journeys in a block of four calendar years. The current block runs from 1 January 2022 to 31 December 2025, so FY 2026-27 falls at the start of the next block (2026-2029). One unavailed journey can be carried into the first year of the next block.

Like HRA, LTA is an old-regime-only benefit. For the block-year carry-forward rules and claim documentation, see our LTA exemption guide under Section 10(5).

Section 10(14) Special Allowances

Section 10(14) covers allowances granted either to meet expenses of the office (clause i) or as personal allowances with fixed statutory ceilings (clause ii, detailed in Rule 2BB). The important distinction is that some are exempt to the extent actually spent, while others carry a flat monthly cap regardless of spend.

Children Education Allowance. Exempt at Rs 100 per month per child, for a maximum of two children. This is a flat cap, not a reimbursement of actual school fees. At Rs 1,200 per child per year, the benefit is modest, and it does not stop you from also claiming tuition fees under Section 80C.

Hostel Expenditure Allowance. Exempt at Rs 300 per month per child, again for up to two children, where the child stays in a hostel. It can be claimed alongside the education allowance for the same child.

Uniform Allowance. Exempt to the extent actually spent on the purchase or maintenance of a uniform that the employee is required to wear on duty. There is no fixed cap, but there is also no exemption for the amount not spent.

Transport Allowance for disabled employees. Exempt up to Rs 3,200 per month for an employee who is blind, deaf and dumb, or orthopaedically handicapped with disability of the lower extremities. This is one of the few allowance exemptions that survives in both regimes. The general transport allowance that ordinary employees once claimed (Rs 1,600 per month) was withdrawn when the standard deduction was reintroduced in FY 2018-19, so only the disabled-employee version remains.

Conveyance and travel allowances for duty. Amounts granted to meet conveyance expenditure incurred in performing official duties, or to cover travel and daily expenses on tour or transfer, are exempt to the extent actually spent. These duty-related allowances also survive in both regimes, because they reimburse a cost rather than reward the employee.

Gratuity: Section 10(10)

Gratuity received on retirement, resignation, or death is exempt under Section 10(10). For a non-government employee covered by the Payment of Gratuity Act, 1972, the exemption is the least of:

- Rs 20 lakh (the statutory ceiling)

- Actual gratuity received

- 15 days' salary for each completed year of service (based on last drawn salary)

The Rs 20 lakh ceiling is a lifetime limit aggregated across all employers, not a fresh limit at each job. Gratuity exemption applies in both regimes, because it is a retirement benefit rather than a running allowance.

Leave Encashment: Section 10(10AA)

Leave encashment received at the time of retirement by a non-government employee is exempt under Section 10(10AA). By CBDT Notification No. 31/2023 dated 24 May 2023, the exemption ceiling was raised from the old Rs 3 lakh to Rs 25 lakh, effective for retirements on or after 1 April 2023.

The exempt amount is the least of Rs 25 lakh, the actual leave encashment, ten months' average salary, or the cash equivalent of unavailed leave (capped at 30 days per completed year of service). The Rs 25 lakh is again a lifetime ceiling across employers, and the exemption applies in both regimes. Note that leave encashment received while still in service is fully taxable; only encashment at retirement qualifies. For a full worked calculation, see our leave encashment exemption guide under Section 10(10AA).

Meal Coupons and Commuted Pension

Meal or food coupons provided by the employer are treated as a perquisite valued at nil up to Rs 50 per meal, for a maximum of two meals per working day, under Rule 3(7)(iii). Anything above that is a taxable perquisite. This concession is tied to perquisite valuation under the old regime.

Commuted pension (a lump sum received by commuting part of your pension) is exempt under Section 10(10A). For a non-government employee, one-third of the commuted value is exempt if gratuity is also received, and one-half is exempt if it is not. This retirement exemption applies in both regimes.

Old Regime vs New Regime: Which Allowances Survive

This is the decision that governs everything above. The new regime under Section 115BAC is now the default; you must actively opt out to claim HRA, LTA, and most Section 10(14) allowances. The grid below shows exactly what carries over.

Comparison

Allowance Exemptions: Old Regime vs New Regime

What you keep if you default into the new regime under Section 115BAC

| Parameter | Old Regime | New Regime (115BAC) |

|---|---|---|

| HRA (Section 10(13A)) | Exempt (least of three) | Fully taxable |

| LTA (Section 10(5)) | Exempt (2 per block) | Fully taxable |

| Children education / hostel allowance | Rs 100 / Rs 300 per child | Fully taxable |

| Meal coupons (Rule 3(7)(iii)) | Rs 50 per meal exempt | Taxable |

| Transport allowance (disabled) | Rs 3,200/month exempt | Rs 3,200/month exempt |

| Conveyance / travel on duty | Exempt (actual spend) | Exempt (actual spend) |

| Gratuity / leave encashment | Rs 20L / Rs 25L exempt | Rs 20L / Rs 25L exempt |

| Standard deduction | Rs 50,000 | Rs 75,000 |

Takeaway: If your salary carries substantial HRA, LTA, and structured allowances, the old regime usually wins. If you rent little or nothing and have few exemptions, the new regime's wider slabs and Rs 75,000 standard deduction often win.

Source: Sections 10(5), 10(10), 10(10AA), 10(13A), 10(14), 115BAC; incometaxindia.gov.in

The break-even framing

Think of it as a single comparison. The new regime hands you a fixed advantage: wider slabs and a Rs 75,000 standard deduction against Rs 50,000 in the old regime. To beat that, your old-regime exemptions and deductions must together exceed the break-even point.

For a metro employee paying real rent, HRA alone can exempt a large slice of salary, and adding LTA, 80C, and 80D usually tips the balance to the old regime. For a young employee living with family, paying no rent, and saving little, the exemptions never accumulate enough to overtake the new regime's built-in advantage, so the default wins. The only way to know your own answer is to compute both. A structured salary that maximises exempt allowances is worthless if you then default into the regime that ignores them. See our guide on salary and CTC restructuring for FY 2026-27 for how to align the two decisions.

How to Claim These Exemptions in Your ITR

Exempt allowances flow through Form 16 into your return, but the responsibility to substantiate them is yours:

- Declare to your employer in advance. HRA, LTA, and Section 10(14) allowances are best captured through employer declarations and proofs (rent receipts, travel tickets, uniform bills) so that they appear as exempt in Form 16 Part B.

- Report the salary components correctly in the ITR. In the salary schedule, gross salary is reduced by the exempt allowances under Section 10. Ensure the figures match Form 16; mismatches reduce your exposure to notices under Section 143(1).

- Choose the regime deliberately. The new regime is the default. If the old regime is better for you and you have business income, you must file Form 10-IEA to opt out within the due date. Salaried taxpayers without business income can switch each year in the return itself.

- Retain evidence. Keep rent receipts, the landlord's PAN where annual rent exceeds Rs 1,00,000, travel tickets, and bills for at least the period the return can be reopened.

Let Tax Garden Structure and File It Right

Getting the exemptions right is a two-step exercise: structure the salary so the exempt components are actually present, then choose the regime that recognises them. Miss either step and the benefit evaporates.

Tax Garden reviews your salary structure against every statutory limit in this guide, computes your liability under both regimes side by side, and files the return that leaves the most in your hands. If your Form 16 has treated an allowance incorrectly, we flag it before it becomes a notice.

Frequently Asked Questions

Can I claim HRA and LTA exemption under the new tax regime?

No. HRA under Section 10(13A) and LTA under Section 10(5) are available only under the old regime. Since the new regime under Section 115BAC is the default from FY 2023-24 onwards, you must actively opt for the old regime to claim them. Under the new regime, both HRA and LTA are fully taxable.

Is Bengaluru or Hyderabad a metro city for HRA purposes?

No. For HRA under Section 10(13A) read with Rule 2A, only Delhi, Mumbai, Kolkata, and Chennai qualify as metro cities for the 50% rate. Bengaluru, Hyderabad, Pune, Gurugram, and all other cities are treated as non-metro and capped at 40% of salary.

What is the exemption limit on gratuity and leave encashment for FY 2026-27?

For non-government employees, gratuity is exempt up to Rs 20 lakh under Section 10(10), and leave encashment at retirement is exempt up to Rs 25 lakh under Section 10(10AA) following CBDT Notification 31/2023. Both are lifetime ceilings across all employers, and both apply under the old and new regimes.

How much children education and hostel allowance is tax-free?

Children education allowance is exempt at Rs 100 per month per child, and hostel expenditure allowance at Rs 300 per month per child, each for a maximum of two children, under Section 10(14) read with Rule 2BB. These are flat caps available only in the old regime, separate from the Section 80C tuition-fee deduction.

Which allowance exemptions survive in the new tax regime?

The transport allowance for blind, deaf-dumb, or orthopaedically handicapped employees (Rs 3,200/month), conveyance and travel allowances incurred for official duty or transfer, and the statutory retirement exemptions for gratuity, leave encashment, and commuted pension all continue under the new regime. HRA, LTA, and the personal Section 10(14) allowances do not.

Are meal or food coupons still tax-free?

Yes, but only under the old regime and only up to Rs 50 per meal for a maximum of two meals per working day, valued under Rule 3(7)(iii). Any amount above that is a taxable perquisite. Under the default new regime, this concession is not available.

Sources: The exemption limits and conditions in this guide are drawn from the Income Tax Act, 1961 and the Income Tax Rules, 1962 as published on the Income Tax Department portal (incometaxindia.gov.in), covering Sections 10(5), 10(10), 10(10A), 10(10AA), 10(13A), 10(14), and 115BAC, along with Rules 2A, 2B, 2BB, and 3(7)(iii). The Rs 25 lakh leave encashment ceiling is per CBDT Notification No. 31/2023 dated 24 May 2023. The LTA block of 1 January 2022 to 31 December 2025 is per Rule 2B. Figures are current as of July 2026; verify against the latest notifications before filing, as allowance limits are periodically revised.