Key Takeaways

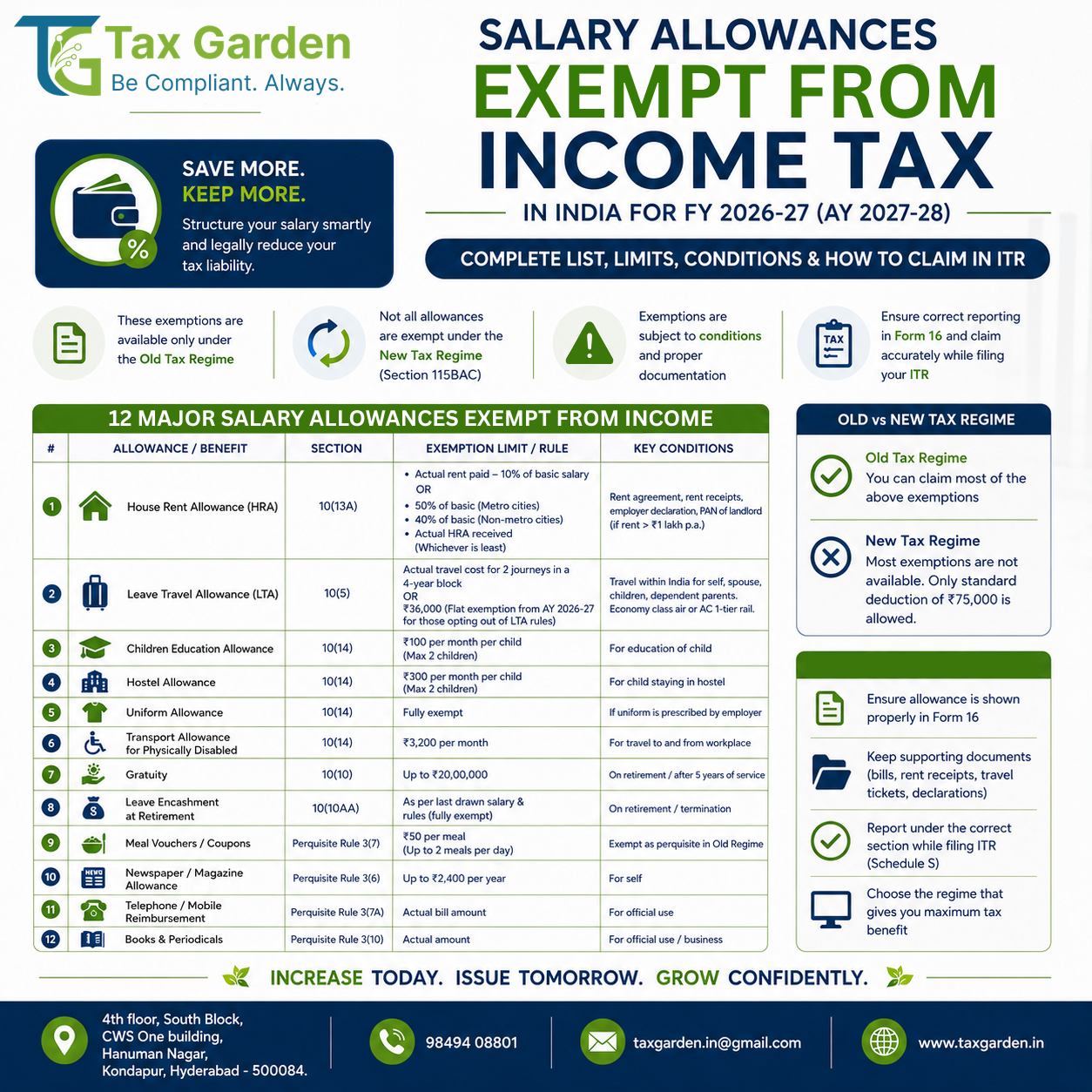

- Government employees get full exemption on leave encashment received at the time of retirement. No monetary ceiling applies.

- Private employees can claim exemption on retirement or resignation, limited to the least of four amounts, with a lifetime cap of Rs 25,00,000 (CBDT Notification 31/2023, effective April 1, 2023).

- Leave encashment received during employment (while still in service) is fully taxable as salary. Section 10(10AA) does not apply.

- The Rs 25 lakh ceiling is a lifetime aggregate across all employers. If you claimed Rs 10 lakh exemption at one employer and resign from the next, only Rs 15 lakh of headroom remains.

- Section 10(10AA) exemption is available under both the old and new tax regimes.

- ITR filing deadline for AY 2026-27 (salaried individuals): July 31, 2026.

Leave encashment is one of the most common components of a retirement or resignation payout for salaried employees in India. Yet it is also one of the most misunderstood. Most employees know that "some exemption" is available. Few know that the exemption is restricted to a specific event (retirement or resignation), capped at the least of four separate amounts, and tracked on a lifetime basis across every employer they have ever worked for.

This guide covers Section 10(10AA) of the Income Tax Act end to end: who qualifies, how to compute the exempt amount, the four-component formula for private employees, the treatment of leave encashment during service, and how to report it correctly in your ITR for AY 2026-27.

Looking for expert help with leave encashment tax exemption calculation Section 10(10AA) AY 2026-27? The team at Tax Garden, based in Kondapur, Hyderabad, helps Indian SMEs stay compliant end-to-end: filings, notices, and advisory, all in one place.

What Is Leave Encashment?

Leave encashment is a cash payment made by an employer to an employee for earned leave (also called privilege leave or annual leave) that the employee has accumulated but not used. The payment can happen in two situations:

- During employment: The employer periodically encashes unutilised leave while the employee is still working. Many companies allow this annually or semi-annually.

- On retirement, resignation, or death: The employer pays out the accumulated leave balance as part of the full and final settlement.

The tax treatment of these two situations is completely different. Only the second category qualifies for exemption under Section 10(10AA).

Government vs Private Employees: The Fundamental Split

Comparison

Leave Encashment Tax Treatment: Government vs Private Employees

| Parameter | Government Employees | Private (Non-Government) Employees |

|---|---|---|

| Exemption on retirement | Fully exempt, no monetary ceiling | Exempt up to the least of 4 amounts (Rs 25 lakh lifetime cap) |

| Exemption during service | Not exempt; taxable as salary | Not exempt; taxable as salary |

| Governing provision | Section 10(10AA)(i) | Section 10(10AA)(ii) |

| Lifetime aggregate limit | None | Rs 25,00,000 across all employers |

| Leave accumulation cap for formula | Not applicable (full exemption) | Maximum 30 days of earned leave per year of service |

| Tax regime applicability | Both old and new regime | Both old and new regime |

Takeaway: Government employees receive full exemption with no ceiling. Private employees must compute the least of four amounts, subject to a Rs 25 lakh lifetime cap.

Government Employees

For employees of the Central Government, State Governments, and local authorities, leave encashment received at the time of retirement (including superannuation) is fully exempt from income tax under Section 10(10AA)(i). There is no monetary ceiling. If a retiring government officer receives Rs 30 lakh as leave encashment, the entire amount is exempt.

Private (Non-Government) Employees

For all other employees, exemption under Section 10(10AA)(ii) is available only on retirement or resignation, and only to the extent of the least of the following four amounts.

The Four-Component Formula for Private Employees

The exempt amount is the lowest of:

| Component | Formula | What It Captures |

|---|---|---|

| 1. Actual leave encashment | The amount actually received from the employer | The real payout |

| 2. Rs 25,00,000 | Statutory ceiling (CBDT Notification 31/2023) | Lifetime aggregate cap across all employers |

| 3. Cash equivalent of unutilised earned leave | (Earned leave entitlement: max 30 days per year of service, minus leave actually taken) x average daily salary | Leave you could have accumulated but did not use |

| 4. 10 months' average salary | 10 x average monthly salary (basic + DA only, averaged over last 10 months) | A salary-linked upper bound |

"Salary" for this purpose means basic pay plus dearness allowance (if DA forms part of retirement benefits). It does not include HRA, bonus, commission, or other allowances.

The leave accumulation for Component 3 is capped at 30 days of earned leave per completed year of service. Even if your company allows 45 days of annual leave, the tax formula caps it at 30.

Worked Example 1: Standard Resignation After 15 Years

Priya resigns from a private company after 15 years and 4 months of service. Her details at the time of resignation:

- Basic salary (last 10 months average): Rs 85,000 per month

- DA: Rs 15,000 per month (forms part of retirement benefits)

- Total salary for formula: Rs 1,00,000 per month

- Leave entitlement per year: 30 days (company policy allows 30)

- Total leave earned: 30 x 15 = 450 days (completed years only)

- Leave actually taken during service: 180 days

- Unutilised leave: 450 - 180 = 270 days

- Actual leave encashment received: Rs 12,50,000

Apply the four tests:

- Actual leave encashment received: Rs 12,50,000

- Statutory ceiling: Rs 25,00,000

- Cash equivalent of unutilised leave: 270 days x (Rs 1,00,000 / 30) = 270 x Rs 3,333.33 = Rs 9,00,000

- 10 months' average salary: 10 x Rs 1,00,000 = Rs 10,00,000

The least of the four is Rs 9,00,000 (Component 3).

Priya's exempt leave encashment: Rs 9,00,000. The remaining Rs 3,50,000 (Rs 12,50,000 minus Rs 9,00,000) is taxable as salary.

Worked Example 2: Senior Executive Hitting the Rs 25 Lakh Ceiling

Rajesh retires from a multinational after 28 years. His details:

- Average monthly salary (basic + DA, last 10 months): Rs 3,50,000

- Leave entitlement per year: 30 days (formula cap)

- Leave actually taken: 300 days

- Unutilised leave: (30 x 28) - 300 = 840 - 300 = 540 days

- Actual leave encashment received: Rs 63,00,000

- Prior employer exemption claimed: Rs 0 (first time claiming)

Apply the four tests:

- Actual leave encashment: Rs 63,00,000

- Statutory ceiling: Rs 25,00,000

- Cash equivalent of unutilised leave: 540 x (Rs 3,50,000 / 30) = 540 x Rs 11,666.67 = Rs 63,00,000

- 10 months' average salary: 10 x Rs 3,50,000 = Rs 35,00,000

The least is Rs 25,00,000 (Component 2, the statutory ceiling).

Exempt amount: Rs 25,00,000. Taxable leave encashment: Rs 63,00,000 minus Rs 25,00,000 = Rs 38,00,000, added to salary income.

Worked Example 3: Lifetime Aggregate Across Two Employers

Meera received Rs 8,00,000 as leave encashment (fully exempt) when she resigned from her first employer in 2024. She now resigns from her second employer in 2026 and receives Rs 22,00,000.

Her remaining lifetime ceiling: Rs 25,00,000 minus Rs 8,00,000 = Rs 17,00,000.

Even if the other three components yield a higher figure, Meera's exemption at the second employer cannot exceed Rs 17,00,000. The balance of Rs 5,00,000 is taxable as salary.

Practical tip: When you resign from an employer and claim leave encashment exemption, note the exempt amount in your personal records. There is no centralised government database tracking the lifetime aggregate. The Income Tax Department reconstructs it from your prior ITR filings. If you fail to report it accurately, a mismatch may surface years later when you claim exemption at a subsequent employer.

Leave Encashment During Employment: Fully Taxable

This is the point most employees miss. If your employer encashes your accumulated leave while you are still in service (for example, an annual leave surrender or a mid-year encashment), that amount is fully taxable as salary income. Section 10(10AA) does not apply.

There is no exemption, no four-component test, and no Rs 25 lakh ceiling. The employer deducts TDS under Section 192 on the full amount, and it appears as part of your gross salary on Form 16.

The only practical relief available during employment is a deduction under Section 89(1) read with Rule 21A, if the encashment relates to leave earned in earlier years. Section 89(1) provides relief for salary arrears or payments that pertain to prior years, but it reduces the tax burden only marginally. It does not make the amount exempt.

Common mistake: Many employees assume that annual leave encashment during service qualifies for Section 10(10AA). It does not. Only leave encashment on retirement, resignation, or termination qualifies. If your employer has been applying an exemption on mid-year encashment on Form 16, the claim is incorrect and may attract a notice.

Common Mistakes That Lead to Incorrect Claims

1. Confusing "During Service" and "On Retirement"

The most frequent error. An employee receives leave encashment in December while still employed, treats it as exempt, and enters a Section 10(10AA) exemption in the ITR. The assessing officer disallows the claim, adds it back to income, and charges interest under Section 234B for shortfall in advance tax. The rule is binary: during service means fully taxable, on exit means the four-component test applies.

2. Using Total Salary Instead of Basic + DA

The formula uses only basic salary plus dearness allowance. Some employees (and even some employers in Form 16) mistakenly use gross salary or CTC. This inflates the Component 4 figure (10 months' average salary) and may inflate the exempt amount. The correct base is basic pay plus DA only, excluding HRA, special allowance, bonus, and all other components.

3. Not Tracking the Lifetime Aggregate

Employees who switch jobs every 3 to 5 years may receive leave encashment at multiple exits. Each time, the four-component test is applied fresh, but the Rs 25 lakh ceiling is cumulative. If you do not track prior claims, you risk overclaiming and receiving a demand notice. Keep a running record of leave encashment exemptions claimed in each year's ITR.

4. Assuming Casual Leave and Sick Leave Count

The exemption formula applies to earned leave (also called privilege leave) only. Casual leave and sick leave are not part of the Section 10(10AA) calculation. If your employer encashes unused sick leave separately, that amount is taxable as salary with no exemption.

5. Ignoring the 30-Day Annual Cap

Even if your company's leave policy grants 35 or 40 days of earned leave per year, the tax formula caps accumulation at 30 days per completed year of service. The excess leave may be encashed by the employer, but the exemption formula does not cover it.

The Rs 25 Lakh Ceiling: CBDT Notification 31/2023

Before May 24, 2023, the exemption limit for non-government employees was Rs 3,00,000. This limit had not been revised since 2002 and was severely outdated relative to current salary levels.

CBDT Notification No. 31/2023, dated May 24, 2023, increased the ceiling to Rs 25,00,000, effective retrospectively from April 1, 2023 (FY 2023-24 onward). Key points:

- The Rs 25 lakh limit applies to leave encashment received on or after April 1, 2023.

- If you retired before April 1, 2023, the old Rs 3 lakh limit applies to your payout.

- The Rs 25 lakh is a lifetime aggregate across all employers. The Income Tax Department tracks this through your ITR filings.

- This notification was issued under the powers conferred by Section 10(10AA)(ii) of the Income Tax Act, 1961.

Old Regime vs New Regime: Section 10(10AA) Applies to Both

Unlike HRA exemption (Section 10(13A)), which is available only under the old regime, the leave encashment exemption under Section 10(10AA) is available under both tax regimes:

- Old regime (Section 115BAC opt-out): Exemption applies. You can also claim other deductions (80C, 80D, etc.).

- New regime (Section 115BAC, default from AY 2024-25): Exemption applies. Section 10(10AA) is specifically listed among the exemptions that survive under the new regime.

This means you do not need to choose the old regime just to claim leave encashment exemption. The exemption works identically under both.

How to Report Leave Encashment in Your ITR

Step-by-Step Guide

Leave Encashment ITR Reporting Checklist

Steps to correctly report leave encashment exemption in your AY 2026-27 ITR

Check Form 16 Part B

Verify whether your employer has reported the leave encashment under gross salary and applied the Section 10(10AA) exemption. If the employer did not apply the exemption, you can claim it yourself in the ITR.

VerificationCompute the exempt amount

Apply the four-component formula. Determine the least of: actual amount received, Rs 25 lakh (minus any prior exemption), cash equivalent of unutilised leave (30 days per year cap), and 10 months' average salary.

CalculationEnter in Schedule Salary

Report the full leave encashment as part of gross salary. Then enter the exempt portion under 'Allowances exempt under Section 10' with the specific sub-section 10(10AA).

ITR EntryCross-check with AIS/TIS

Verify the leave encashment amount in your Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) on the income tax portal. Flag any mismatch before filing.

ReconciliationRetain documentation

Keep the full and final settlement letter, leave balance certificate, and salary slips for the last 10 months. These are needed if the assessing officer questions the exemption claim.

RecordsSource: Section 10(10AA), Income Tax Act; ITR-1/ITR-2 Schedule Salary instructions

In ITR-1 (Sahaj) and ITR-2, the leave encashment exemption is entered under the salary schedule:

- Gross salary includes the full leave encashment amount.

- Allowances exempt under Section 10 includes the computed exempt amount under Section 10(10AA).

- The difference flows into net taxable salary.

If you are filing ITR-1, the form provides a specific line for Section 10 exemptions. In ITR-2, Schedule Salary has a detailed breakup where you enter each exemption with its section reference.

Documents to Keep Ready

Before filing, gather these documents for your records and potential scrutiny:

- Full and final settlement letter from your employer, showing the leave encashment amount separately

- Leave balance certificate or leave ledger printout confirming accumulated and utilised leave

- Salary slips for the last 10 months before exit, showing basic pay and DA breakup

- Form 16 (or Form 130 from Tax Year 2026-27) reflecting the leave encashment and any exemption applied by the employer

- Prior ITRs where you claimed Section 10(10AA) exemption (for lifetime aggregate tracking)

- Appointment letter or HR confirmation of the annual earned leave entitlement under company policy

These are not submitted with the ITR but must be available if the assessing officer raises a query or issues a notice under Section 143(1) or Section 143(2).

Leave Encashment on Death of an Employee

When an employee dies in service and the employer pays leave encashment to the legal heirs or nominees, the treatment is favourable:

- Several ITAT rulings have held that leave encashment received by legal heirs on the death of the employee is not taxable in the hands of the heirs. The rationale: the heirs are not "employees" and the payment is in the nature of a capital receipt.

- For government employees, the full exemption under Section 10(10AA)(i) applies, and the death scenario does not create any taxable event.

- For private employees, while the legal position from ITAT precedents supports full exemption, it is prudent to declare the receipt in the ITR and claim exemption, keeping the settlement letter and death certificate as documentation.

Income Tax Act 2025: What Changes?

The Income Tax Act 2025, effective from April 1, 2026, consolidates and rationalises the Income Tax Act 1961. For leave encashment:

- The substantive exemption continues. The Rs 25 lakh ceiling, the four-component formula, and the government employee full exemption remain intact.

- Section numbering may change. The 2025 Act reorganises sections. Practitioners should verify the new section number corresponding to the old Section 10(10AA) when filing for Tax Year 2026-27 (AY 2027-28 equivalent). For AY 2026-27 (FY 2025-26), the old Act still governs.

- All ITR forms for AY 2026-27 reference the old section numbers. No action is needed for this filing year.

Looking for expert help with leave encashment exemption ITR filing AY 2026-27 salaried employees? The team at Tax Garden, based in Kondapur, Hyderabad, helps Indian SMEs stay compliant end-to-end: filings, notices, and advisory, all in one place.

Where Tax Garden Helps

Leave encashment calculations involve multiple variables: years of service, leave records, salary components, and the lifetime aggregate tracking across employers. A single error in the four-component test can lead to either overclaiming (which triggers a notice) or underclaiming (which means you pay more tax than necessary).

Tax Garden's ITR filing service includes a full leave encashment review as part of every return: we compute all four components, reconcile with Form 16 and AIS, track the lifetime aggregate, and file the return with the correct Section 10(10AA) claim. If you are changing jobs or retiring this year, our CAs ensure the full and final settlement is reported correctly.

Frequently Asked Questions

Is leave encashment during employment exempt from tax?

No. Leave encashment received while you are still employed is fully taxable as salary income. Section 10(10AA) exemption applies only on retirement, resignation, or termination. The only partial relief during employment is Section 89(1) for arrears pertaining to earlier years.

What is the current exemption limit for leave encashment?

For non-government employees, the lifetime exemption ceiling is Rs 25,00,000, raised from Rs 3,00,000 by CBDT Notification 31/2023 effective April 1, 2023. For government employees (central, state, local authority), leave encashment on retirement is fully exempt with no monetary limit.

Does the Rs 25 lakh limit apply per employer or per lifetime?

Per lifetime, across all employers combined. If you claimed Rs 10 lakh exemption at your first employer, only Rs 15 lakh of exemption headroom remains at subsequent employers. The Income Tax Department tracks cumulative claims through your ITR history.

Is leave encashment exemption available under the new tax regime?

Yes. Section 10(10AA) is one of the exemptions specifically preserved under the new tax regime (Section 115BAC). You do not need to switch to the old regime to claim leave encashment exemption.

What salary components are included in the 10-month average salary calculation?

Only basic salary and dearness allowance (DA, if it forms part of retirement benefits). HRA, bonus, commission, overtime, and other allowances are excluded from the calculation.

How is the 30-day leave cap applied in the formula?

The tax formula caps earned leave accumulation at 30 days per completed year of service, regardless of your company's leave policy. If your employer grants 40 days of earned leave per year, the exemption formula still uses 30. The difference may be encashed but the exemption does not cover it.

What happens if my employer did not apply the exemption on Form 16?

You can claim the exemption directly in your ITR. Report the full leave encashment as gross salary, then enter the exempt amount under Section 10(10AA) in the salary schedule. Keep your full and final settlement letter and leave balance certificate as supporting documentation.

Is leave encashment received by legal heirs on death of the employee taxable?

Based on multiple ITAT rulings, leave encashment paid to legal heirs on the death of an employee is generally treated as a non-taxable capital receipt. However, it is prudent to declare it in the ITR and claim exemption with the settlement letter and death certificate as documentation.

Work with the Trusted Tax & Compliance Services in Kondapur, Hyderabad - Tax Garden for expert GST filing, ITR, TDS, ROC, and startup compliance support.

Frequently Asked Questions: Tax Services in Kondapur & Hyderabad

What makes Tax Garden a preferred GST consultant in Kondapur?

Tax Garden is ISO 9001:2015 certified and backs every engagement with Kavach, our ₹50,000 error-protection cover. Our flat-fee, no-surprise pricing and dedicated account manager make us a compliance partner for startups and SMEs in Kondapur's HITEC City corridor.

Why is Tax Garden a trusted tax compliance partner in Hyderabad?

Trust comes from three pillars at Tax Garden. First, transparency: you know the exact fee before you sign up, and it never changes mid-year. Second, certified expertise: our compliance team is qualified, and the firm holds ISO 9001:2015 certification. Third, accountability: Kavach, our unique error-protection plan, covers up to ₹50,000 in service charges for any clerical mistake made by our team.

Is there a reliable tax consultant near me in Kondapur?

Yes. Tax Garden's office is in Kondapur itself (CWS One Building, Hanuman Nagar). You can book an in-person consultation or get everything done fully online via WhatsApp and our client portal. We serve walk-in clients by appointment and remote clients across all of Hyderabad and Telangana.

I want a friendly CA who explains things clearly. Is that Tax Garden?

Absolutely. Every client gets a dedicated account manager reachable on WhatsApp, plain-language explanations of what is filed and why, and proactive reminders before every deadline. No jargon, no surprises, just friendly, expert compliance support from Kondapur.

Where is Tax Garden located in Hyderabad?

Tax Garden is located at 4th Floor, South Block, CWS One Building, Hanuman Nagar, Kondapur, Hyderabad, Telangana 500084. We serve clients across Kondapur, HITEC City, Gachibowli, Madhapur, Jubilee Hills, Banjara Hills, and all of Hyderabad.

Can I get GST filing and registration services in Kondapur?

Yes. Tax Garden offers end-to-end GST services from our Kondapur office: GST registration, GSTR-1, GSTR-3B, GSTR-9 annual returns, ITC reconciliation, e-invoicing setup, and GST notice handling for businesses of all sizes in Kondapur and Hyderabad.

Do you file ITR for salaried employees and businesses in Hyderabad?

Yes. Our Kondapur team files ITR for salaried employees, freelancers, consultants, business owners, LLPs, and companies across Hyderabad. We cover ITR-1 through ITR-6 with complete Chapter VI-A deduction reconciliation, AIS reconciliation, and proactive deadline management.

Which areas in Hyderabad does Tax Garden serve?

Tax Garden's Kondapur office serves clients across Hyderabad including HITEC City, Gachibowli, Madhapur, Jubilee Hills, Banjara Hills, Begumpet, Secunderabad, Ameerpet, Kukatpally, Uppal, LB Nagar, and all of Telangana. Most services are available fully online.

What compliance services does Tax Garden offer for startups in Kondapur?

Tax Garden is a compliance partner for startups in Kondapur and Hyderabad's HITEC City corridor. We handle company incorporation, GST registration, TDS filings, payroll, ROC annual filings, director KYC, and annual ITR filing, all under one flat-fee plan.

How is Tax Garden different from traditional accountants and tax firms in Hyderabad?

Unlike traditional accounting practices that charge hourly and are difficult to reach, Tax Garden operates on flat-fee subscription plans with a dedicated account manager, monthly compliance updates, and WhatsApp-first communication. Our AI-powered workflow catches errors before filings are submitted, and Kavach error-protection ensures you are never left alone if something goes wrong.

Sources

This guide is verified against Section 10(10AA) of the Income Tax Act, 1961 (carried forward under the Income Tax Act, 2025), CBDT Notification No. 31/2023 dated May 24, 2023 (raising the exemption limit from Rs 3,00,000 to Rs 25,00,000 effective April 1, 2023), Rule 2BA of the Income Tax Rules, and the latest ITR form instructions published on incometax.gov.in/iec/foportal/ for AY 2026-27. Government employee full exemption is per Section 10(10AA)(i). The 30-day-per-year leave accumulation cap and 10-month salary formula are codified in Section 10(10AA)(ii) read with Rule 2BA. ITAT rulings on death-related leave encashment were reviewed for the legal heir exemption position. Always validate the specific figures against your full and final settlement letter, Form 16, and leave records before filing.