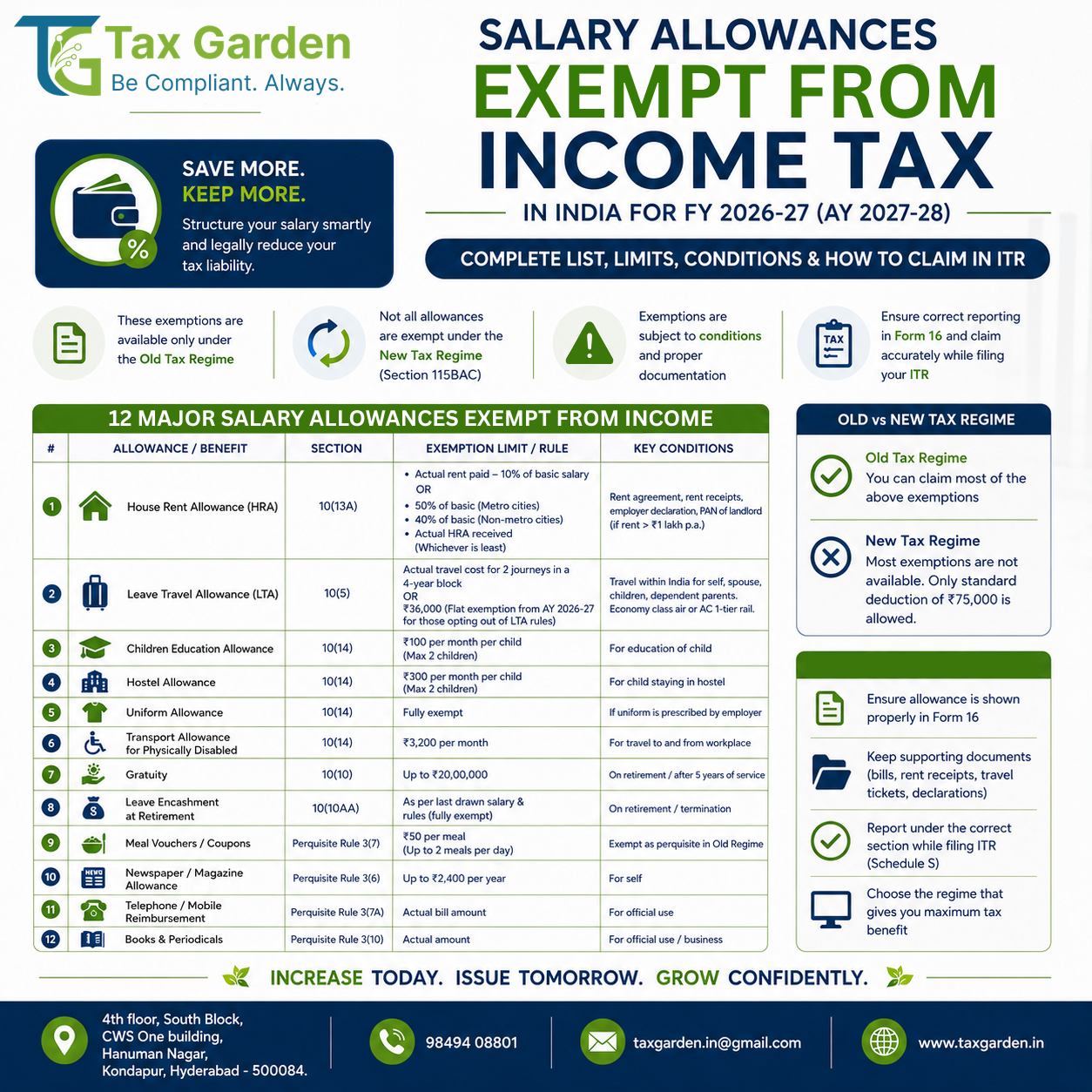

Key Takeaways

- TDS refund can only be claimed by filing your Income Tax Return (ITR). There is no separate refund application.

- Common triggers: excess salary TDS without investment proof submission, TDS on FD interest for taxpayers below the taxable threshold, and TDS on rent exceeding actual liability.

- Refund is credited to your pre-validated bank account linked on the e-filing portal. Pre-validation is mandatory.

- Under Section 244A, you earn simple interest at 0.5% per month (6% per annum) on delayed refunds.

- Refunds up to Rs 50,000 are processed centrally by CPC without Assessing Officer approval.

- E-verification within 30 days of filing is mandatory: without it, no refund is processed.

- Outstanding demands under Section 245 can be adjusted against your refund before release.

If your employer deducted TDS on your full salary but you actually have deductions under Section 80C, 80D, or HRA exemption that bring your tax liability below the TDS already deducted, the excess amount sits with the government until you file your ITR and claim it back. This guide walks you through the entire process of claiming your TDS refund for AY 2026-27: from identifying excess deduction to receiving the credit in your bank account.

Looking for expert help with how to claim TDS refund online India AY 2026-27 ITR filing process? The team at Tax Garden, based in Kondapur, Hyderabad, helps Indian SMEs stay compliant end-to-end: filings, notices, and advisory, all in one place.

What Is a TDS Refund?

A TDS refund is the difference between the total TDS deducted from your income during the financial year and your actual tax liability computed after applying all deductions, exemptions, and rebates. When TDS deducted exceeds your final tax payable, the excess amount is refundable by the Income Tax Department.

The refund is not automatic. You must file your ITR, declare all income sources, claim applicable deductions, and demonstrate that TDS already deducted exceeds the computed liability. CPC Bengaluru processes the return, computes the refund, and credits it to your bank.

Common Situations Where Excess TDS Arises

1. Salary TDS Without Investment Proof

Your employer deducts TDS monthly based on your declared investments at the start of the year. If you fail to submit proof (rent receipts, 80C investment statements, insurance premium receipts) before the February deadline, the employer deducts TDS on the full taxable salary without giving credit for those deductions. Your actual liability computed at year-end is lower than the TDS deducted.

2. TDS on Fixed Deposit Interest: Senior Citizens Below Threshold

Banks deduct TDS at 10% on FD interest exceeding Rs 50,000 per year for senior citizens (Rs 40,000 for others). A senior citizen with total income below Rs 5,00,000 (eligible for full rebate under Section 87A) ends up with zero tax liability, making the entire TDS deducted refundable. Filing Form 15H prevents future TDS, but for the year already passed, an ITR claim is the only recourse.

3. TDS on Rent Exceeding Actual Tax Liability

Tenants paying rent above Rs 50,000 per month deduct TDS at 2% under Section 194-IB. For landlords whose total income (after deductions for home loan interest under Section 24, standard deduction of 30%, and other exemptions) falls below the taxable limit, this TDS is fully refundable.

4. Double Deduction Errors and Incorrect TDS Rates

Occasionally, a deductor applies a higher rate (20% instead of 10% due to missing PAN on record, or contractual payment classified under the wrong section). These errors create excess TDS that can only be recovered through ITR filing.

Step-by-Step Process to Claim TDS Refund Through ITR Filing

Follow this sequence precisely:

Step 1: Verify Form 26AS and AIS

Log in to the e-filing portal at incometax.gov.in. Go to e-File and select View Form 26AS (redirects to TRACES). Cross-check every TDS entry: deductor TAN, amount deducted, and quarter. Also check your Annual Information Statement (AIS) under the AIS tab for any mismatches.

Step 2: Download Form 16/16A

Collect Form 16 (salary) from your employer and Form 16A (non-salary TDS) from banks and other deductors. These certificates confirm the TDS deposited to the government against your PAN.

Step 3: Compute Your Total Income and Tax Liability

Add all income heads: salary, house property, capital gains, business/profession, and other sources. Apply deductions (Chapter VI-A: 80C, 80D, 80E, etc.) and exemptions. Compute tax payable under either the old or new regime.

Step 4: Select the Correct ITR Form

| Taxpayer Category | Applicable ITR Form |

|---|---|

| Salaried with salary + FD/savings interest only | ITR-1 (Sahaj) |

| Salaried with capital gains or multiple house properties | ITR-2 |

| Business/profession income (non-presumptive) | ITR-3 |

| Presumptive income under Section 44AD/44ADA | ITR-4 (Sugam) |

Step 5: File the ITR Online

Log in to incometax.gov.in, go to e-File, select Income Tax Returns, and click File Income Tax Return. Choose the correct AY (2026-27), select your ITR form, and fill in all schedules. The portal auto-populates TDS details from Form 26AS. Verify that the pre-filled TDS matches your Form 16/16A. Submit.

Step 6: E-Verify Within 30 Days

E-verification is mandatory. Without it, your return is treated as not filed. Use Aadhaar OTP (fastest), net banking, bank account EVC, or DSC. Do this immediately after filing.

Step 7: Track Refund Status

After e-verification, CPC processes the return and determines the refund. Monitor status using the methods described below.

How to Check TDS Refund Status Online

Method 1: e-Filing Portal (With Login)

- Log in to incometax.gov.in with your PAN and password.

- Navigate to e-File, then Income Tax Returns, then View Filed Returns.

- Select AY 2026-27 and click View Details.

- The status shows: Processing, Processed (Refund Issued), Refund Failed, or Demand Raised.

Method 2: NSDL/Protean Refund Status (Without Login)

- Go to tin.tin.nsdl.com/oltas/refund-status-pan.html.

- Enter your PAN and select AY 2026-27.

- Enter the captcha and submit.

- The page shows refund amount, date of issue, and mode of payment.

This method is quick but provides limited detail. For failure reasons or demand adjustments, use the e-filing portal.

Refund Processing Timeline

| Stage | Expected Timeline |

|---|---|

| ITR filing to e-verification | Immediately (same day recommended) |

| CPC processing after e-verification | 15 to 30 days |

| Refund credit to bank account | 20 to 45 days from e-verification |

| Peak season delays (July to October filings) | Up to 60 days |

Returns filed early in the season (before July 15) and e-verified on the same day typically receive refunds within 15 to 20 days. Returns filed on the last date face batch-processing queues.

Section 244A: Interest on Delayed Refund

If the department delays your refund beyond the normal processing period, you are entitled to simple interest at 0.5% per month (6% per annum) under Section 244A of the Income Tax Act.

Interest calculation rules:

- If ITR is filed on or before the due date (July 31 for non-audit): interest runs from April 1 of the assessment year to the date of refund grant.

- If ITR is filed after the due date (belated return): interest runs from the date of filing to the date of refund grant.

- Interest is computed on simple interest basis, not compounded.

- No interest is paid for any delay attributable to the taxpayer (incorrect details, non-response to notices).

Example: You file ITR on July 20, 2026, claiming a refund of Rs 1,00,000. E-verification is done on July 20. If the refund is credited on December 20, 2026 (5 months from July 20, but interest calculated from April 1, 2026, since filed before due date): interest = Rs 1,00,000 x 0.5% x 9 months (April to December) = Rs 4,500.

Reasons Your TDS Refund Gets Rejected or Delayed

| Reason | Fix |

|---|---|

| Bank account not pre-validated | Pre-validate your bank account on the e-filing portal before filing |

| PAN and bank account name mismatch | Update name on PAN or bank account to match exactly |

| Incorrect ITR form selected | File a revised return with the correct form before the deadline |

| TDS claimed does not match Form 26AS | Contact deductor to file TDS correction return |

| Outstanding demand exists (Section 245) | Respond to the Section 245 intimation: agree, disagree, or file rectification |

| Return not e-verified within 30 days | E-verify immediately using Aadhaar OTP or other modes |

| Invalid or closed bank account | Add and pre-validate a new active bank account, then raise refund re-issue request |

If you receive a Section 245 intimation stating your refund will be adjusted against a prior-year demand, respond within 30 days. If you disagree with the demand, file a rectification under Section 154 before the adjustment deadline passes.

Tips to Get Your TDS Refund Faster

- Pre-validate your bank account before filing. This is the single most important step. An unvalidated account guarantees a failed refund.

- Verify Form 26AS and AIS match your records. Mismatches between your claimed TDS and the department's records will trigger processing delays or demand notices.

- File early in the season. Returns filed in June or early July get processed faster than those filed on July 31 during the peak rush.

- E-verify immediately after filing. Do not wait. The 30-day clock starts on the filing date, and CPC only begins processing after e-verification.

- Choose the correct ITR form. Filing ITR-1 when you have capital gains income leads to defective return notices and processing delays.

- Keep your email and mobile updated on the portal. Intimation orders, refund confirmations, and demand notices are sent to the registered email and mobile. Outdated contact information means missed communications.

Frequently Asked Questions

Can I claim TDS refund without filing ITR?

No. Filing an Income Tax Return is the only mechanism to claim excess TDS back from the government. There is no separate refund application or form.

How long does a TDS refund take after filing?

Typically 20 to 45 days from the date of e-verification. Early filers (June to early July) often receive refunds within 15 to 20 days.

What if my refund is less than expected?

CPC may have disallowed certain deductions or adjusted the refund against a prior-year demand under Section 245. Check your Section 143(1) intimation order on the e-filing portal for the detailed computation.

Is TDS refund taxable?

The refund amount itself is not taxable (it is return of your own money). However, the interest received under Section 244A on delayed refund is taxable as "Income from Other Sources" in the year of receipt.

Source attribution: This guide references the Income Tax Act, 1961 (Sections 244A, 245, 139, 143), CBDT circulars on refund processing timelines, and the official e-filing portal documentation at incometax.gov.in. TDS rates and thresholds are current as of FY 2025-26 / AY 2026-27.