Key Takeaways

- Every ITR filing for AY 2026-27 (FY 2025-26) requires PAN, Aadhaar, Form 26AS, AIS, and bank statements at a minimum.

- Salaried individuals need Form 16 (or the upcoming Form 130 under the Income Tax Act 2025), Form 12BB, and rent receipts if claiming HRA.

- Business and professional filers must keep profit and loss accounts, balance sheets, GST returns, and audit reports (if applicable) ready.

- Capital gains filers need broker statements (contract notes), CAMS/KFintech statements for mutual funds, and property sale deeds.

- Cross-verify every income source and TDS entry against your AIS/TIS before filing to reduce exposure to penalties and notices.

- Filing deadline: July 31, 2026 for non-audit cases; October 31, 2026 for audit cases.

What documents are required for ITR filing AY 2026-27? You need PAN, Aadhaar, Form 16 (salaried), Form 26AS, Annual Information Statement (AIS), bank statements, investment proofs under Section 80C/80D, and capital gains statements. Business filers additionally need P&L accounts, balance sheets, and GST returns.

Filing your Income Tax Return for Assessment Year 2026-27 (covering income earned during Financial Year 2025-26) requires a well-organised set of documents. Missing even a single form, whether it is a TDS certificate or a capital gains statement, can delay your filing, trigger a defective return notice under Section 139(9), or result in missed deductions that increase your tax liability.

This checklist covers every document category: universal identity proofs, salary-related forms, business records, capital gains evidence, deduction proofs, foreign income disclosures, and the critical AIS/TIS/Form 26AS reconciliation. Whether you are a salaried employee, freelancer, small business owner, or investor, use this as your pre-filing reference.

Looking for expert help with documents required ITR filing AY 2026-27 checklist? The team at Tax Garden, based in Kondapur, Hyderabad, helps Indian SMEs stay compliant end-to-end: filings, notices, and advisory, all in one place.

Universal Documents (All Taxpayers)

Every taxpayer, regardless of income source or ITR form type, must have these documents ready before filing.

| Document | Purpose | Where to Obtain |

|---|---|---|

| PAN Card | Primary tax identifier; mandatory for all returns | NSDL/UTIITSL; linked to Aadhaar |

| Aadhaar Card | Required for e-verification and PAN-Aadhaar linkage (Section 139AA) | UIDAI portal |

| Form 26AS (Annual Tax Statement) | Shows TDS/TCS credits, advance tax, self-assessment tax paid | TRACES portal or Income Tax e-filing portal |

| Annual Information Statement (AIS) | Comprehensive record of all financial transactions reported by third parties | Income Tax e-filing portal under "AIS" tab |

| Taxpayer Information Summary (TIS) | Processed version of AIS with aggregated values used for pre-filling | Income Tax e-filing portal |

| Bank Statements (all accounts) | Interest income, cash deposits, high-value transactions | Net banking or branch request |

| Bank Account Details | Account number, IFSC, bank name for refund credit | Passbook or cheque book |

AIS is now the primary verification document. Starting AY 2025-26, the Income Tax Department relies heavily on AIS data for pre-filling returns and issuing mismatch notices. Always download and reconcile your AIS before filing. If you spot errors, submit feedback on the AIS portal to correct them before the filing date.

Documents for Salaried Individuals

If you earn salary income, these documents form the backbone of your ITR-1 (Sahaj) or ITR-2 filing.

Form 16 (Parts A and B)

Form 16 is the TDS certificate issued by your employer under Section 203. Part A shows TDS deducted and deposited quarter-wise; Part B is a detailed computation of your salary income, exemptions claimed (HRA, LTA), and deductions allowed.

Note on Income Tax Act 2025: The new Act introduces Form 130 as the consolidated TDS certificate format. For AY 2026-27 filings, most employers will still issue Form 16 under the existing framework, but verify with your employer if they have transitioned to Form 130.

Other Salary Documents

| Document | When Required |

|---|---|

| Form 12BB | Investment declaration submitted to employer for TDS calculation |

| Salary Slips (all 12 months) | To verify basic pay, DA, HRA, special allowance breakup |

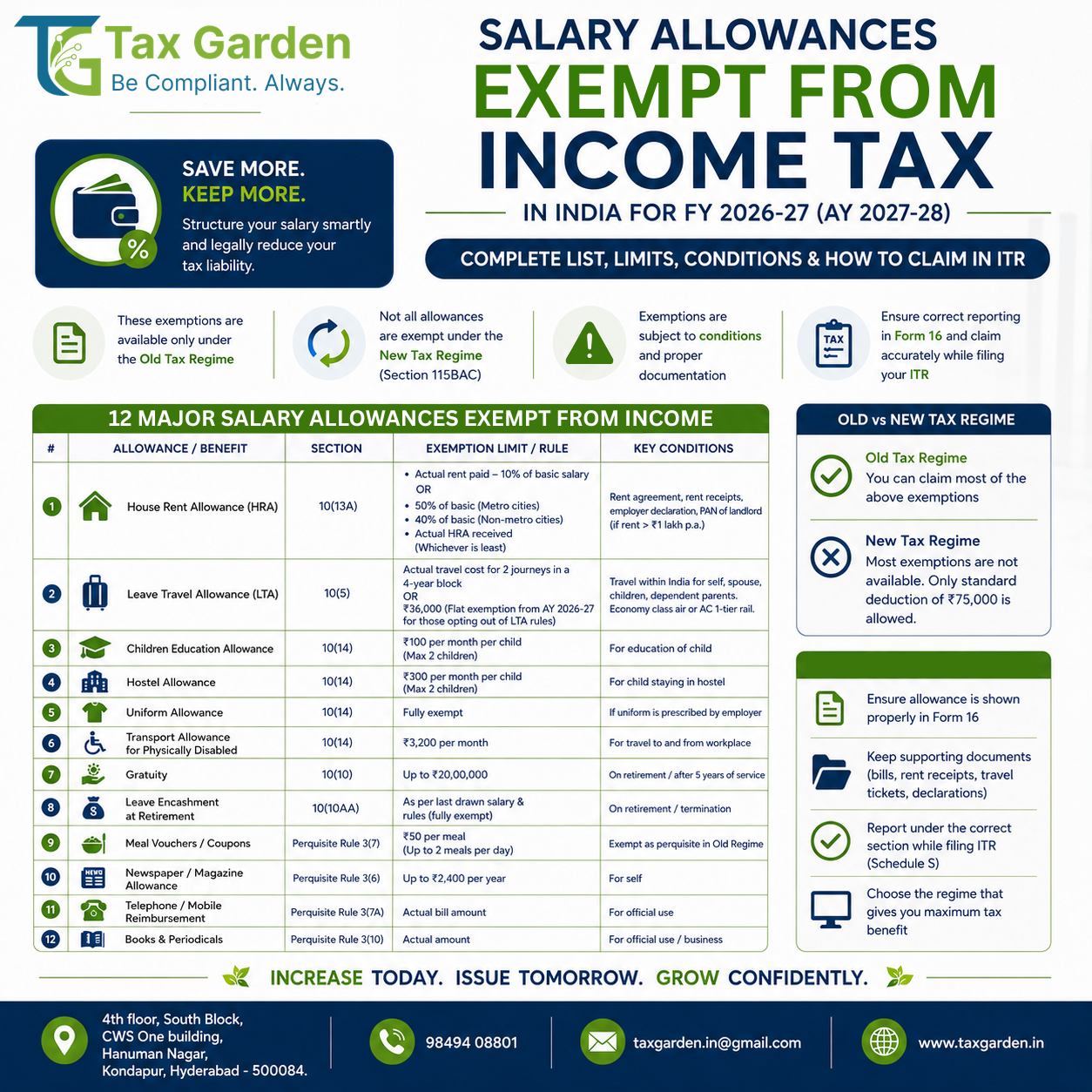

| Rent Receipts + Lease Agreement | If claiming HRA exemption under Section 10(13A) |

| Form 10BA (Declaration for Rent Paid) | If claiming deduction under Section 80GG (no HRA from employer) |

| Leave Travel Allowance (LTA) bills | Travel receipts for LTA exemption claims |

| Employer-issued Perquisite Statement | If employer provides car, accommodation, or other perquisites |

Pro Tip: If you changed jobs during FY 2025-26, collect Form 16 from each employer. Report the combined salary and ensure TDS from all employers is reflected in Form 26AS.

Documents for Business and Professional Income

Taxpayers filing ITR-3 or ITR-4 (Sugam) for business or professional income need accounting records alongside standard documents.

For Regular Business Filers (ITR-3)

- Profit and Loss Account for FY 2025-26

- Balance Sheet as on March 31, 2026

- Cash Flow Statement (if applicable under accounting standards)

- Bank Statements for all business accounts

- Purchase and Sales Invoices (or consolidated summaries)

- GST Returns (GSTR-1, GSTR-3B) for reconciliation with reported turnover

- TDS Certificates (Form 16A) from clients who deducted TDS on payments

- Depreciation Schedule for all fixed assets

- Loan Statements (if claiming interest as a business expense)

For Presumptive Taxation Filers (ITR-4)

If you opt for presumptive taxation under Section 44AD (business) or Section 44ADA (professionals), document requirements are simpler:

- Bank Statements showing gross receipts/turnover

- Gross Receipts Summary or invoicing records

- Form 16A from clients (for TDS reconciliation)

- GST Returns (if registered)

Audit Threshold: If your total turnover exceeds Rs 1 crore (or Rs 10 crore with cash receipts and payments each below 5% of total), a tax audit under Section 44AB is mandatory. Keep your audit report (Form 3CA/3CD or 3CB/3CD) ready. The filing deadline extends to October 31, 2026 for audit cases.

Documents for Capital Gains

Capital gains reporting is one of the most document-intensive areas. Gather evidence for every asset class you traded or sold during FY 2025-26.

Securities (Stocks, Mutual Funds, ETFs)

| Document | Source |

|---|---|

| Broker Contract Notes | Your stockbroker (Zerodha, Groww, Angel One, etc.) |

| Annual Capital Gains Statement | Broker platform's tax P&L section |

| CAMS/KFintech Consolidated Statement | For mutual fund redemptions; request via MyCams or KFintech portal |

| Dividend Statements | Broker or AMC; dividends are taxable as "Income from Other Sources" |

| Demat Account Holding Statement | CDSL/NSDL for verifying acquisition dates and costs |

Real Estate

- Sale Deed of property sold during FY 2025-26

- Purchase Deed (original acquisition) with stamp duty and registration charges

- Cost of Improvement receipts (renovation, construction)

- Fair Market Value (FMV) as on April 1, 2001 if property was acquired before this date (for indexation purposes)

- Form 26QB challan (TDS on property purchase, if buyer deducted 1% TDS)

- Section 54/54EC/54F investment proofs if claiming capital gains exemption (new property purchase deed, 54EC bonds certificate)

Other Capital Assets

- Gold/Jewellery: Purchase receipts or valuation certificates

- Unlisted Shares: Valuation report from a merchant banker (for FMV determination)

- Virtual Digital Assets (VDAs): Transaction history from crypto exchanges; taxed at flat 30% under Section 115BBH with no deductions except cost of acquisition

New Tax Regime Capital Gains Rates (FY 2025-26):

- STCG on listed equity: 20% (increased from 15%)

- LTCG on listed equity: 12.5% (increased from 10%), exemption up to Rs 1.25 lakh

- LTCG on real estate: 12.5% without indexation (indexation benefit removed from July 23, 2024)

Deduction and Exemption Proofs

To claim deductions under Chapter VI-A and other provisions, keep these investment and payment proofs ready.

Section 80C (Up to Rs 1.5 Lakh)

| Investment/Payment | Proof Required |

|---|---|

| Life Insurance Premium | Premium payment receipts or policy statements |

| PPF Contribution | Passbook or account statement |

| ELSS Mutual Funds | CAMS/KFintech statement or AMC statement |

| NSC (National Savings Certificate) | Post office certificate |

| 5-Year Tax-Saving FD | FD receipt from bank |

| Sukanya Samriddhi Account | Passbook or account statement |

| Tuition Fees (up to 2 children) | Fee receipts from school/university |

| Home Loan Principal Repayment | Loan statement from bank/NBFC |

| Stamp Duty and Registration Charges | Payment receipts (year of payment only) |

Section 80CCD (NPS Contributions)

- Section 80CCD(1): Employee contribution to NPS (within 80C limit)

- Section 80CCD(1B): Additional deduction up to Rs 50,000 for NPS

- Section 80CCD(2): Employer contribution to NPS (up to 14% of salary for government employees, 10% for others)

- Proof: NPS Transaction Statement from CRA (NSDL/KFintech)

Section 80D (Health Insurance)

| Category | Deduction Limit | Proof Required |

|---|---|---|

| Self, Spouse, Children | Up to Rs 25,000 | Health insurance premium receipt |

| Parents (below 60) | Up to Rs 25,000 | Premium receipt |

| Parents (60 or above) | Up to Rs 50,000 | Premium receipt |

| Preventive Health Check-up | Up to Rs 5,000 (within 80D limit) | Payment receipt or bill |

Section 24(b): Home Loan Interest

- Home Loan Interest Certificate from lender (mandatory)

- Shows interest paid, principal repaid, and outstanding balance

- Deduction up to Rs 2 lakh for self-occupied property; no limit for let-out property

- Pre-construction Interest Certificate if the home was under construction

Other Deductions

| Section | Deduction For | Proof |

|---|---|---|

| 80E | Education Loan Interest | Loan interest certificate from bank |

| 80EEA | First-time Home Buyer Interest (if applicable) | Loan sanction letter + interest certificate |

| 80G | Donations to eligible trusts/funds | Donation receipt with PAN of donee; 80G certificate |

| 80TTA | Savings Account Interest (up to Rs 10,000) | Bank statement |

| 80TTB | Senior Citizen Interest Income (up to Rs 50,000) | Bank/FD/PO interest certificates |

| 80U | Disability (self) | Disability certificate from prescribed authority |

| 80DD | Disabled Dependent | Medical certificate + expenditure receipts |

Old vs New Tax Regime: Under the new tax regime (default from AY 2024-25 onwards), most Chapter VI-A deductions except Section 80CCD(2) and Section 80JJAA are not available. If you are claiming deductions under 80C, 80D, or 24(b), you must opt for the old regime by filing Form 10-IEA before the due date.

Foreign Income and Asset Documents

If you have any foreign income or hold foreign assets, additional disclosure under Schedule FA (Foreign Assets) and Schedule FSI (Foreign Source Income) is mandatory.

| Document | Purpose |

|---|---|

| Foreign Bank Account Statements | Interest income, balance as on December 31, 2025 |

| Foreign Salary/Pension Statements | If employed abroad or receiving foreign pension |

| Foreign Property Documents | Ownership details, rental income |

| DTAA Certificate / Tax Residency Certificate (TRC) | To claim relief under Double Taxation Avoidance Agreement |

| Foreign Tax Payment Receipts | For claiming credit under Section 90/91 |

| RSU/ESOP Statements from Foreign Employer | Exercise date, FMV, shares acquired, sale details |

Failure to disclose foreign assets can attract penalties of Rs 10 lakh under the Black Money (Undisclosed Foreign Income and Assets) Act, 2015.

AIS, TIS, and Form 26AS: The Reconciliation Trio

Before you begin filling your ITR, reconciling these three documents is the single most important step to ensure accuracy.

What Each Document Shows

| Document | Data Covered | Primary Use |

|---|---|---|

| Form 26AS | TDS/TCS credited, advance tax, self-assessment tax, high-value transactions | Verify tax credits claimed in ITR |

| AIS | Salary, interest, dividends, share transactions, mutual fund purchases/redemptions, property transactions, foreign remittances | Cross-check all reported income sources |

| TIS | Derived/processed values from AIS; shows what the department considers your income | Verify pre-filled ITR values |

Reconciliation Checklist

- Download all three from the Income Tax e-filing portal.

- Match TDS amounts in Form 26AS with your Form 16/16A certificates.

- Verify every AIS entry: interest from each bank account, dividends from each company, mutual fund transactions, property registrations.

- Flag discrepancies: If AIS shows income you did not earn (e.g., incorrect SFT reporting by a bank), submit feedback on the AIS portal before filing.

- Check TIS derived values: The "Processed Value" in TIS may differ from your actual income if you submitted AIS feedback. Ensure TIS reflects corrections.

Common AIS Mismatches: Joint account interest shown entirely in one PAN holder's AIS; incorrect mutual fund transaction values; duplicate SFT entries for the same FD. Always verify and submit feedback for corrections before filing.

Pre-Filing Document Organisation Checklist

Use this consolidated checklist before sitting down to file.

Step 1: Identity and Access

- PAN Card (linked to Aadhaar)

- Aadhaar Card

- Income Tax e-filing portal login credentials

- Bank account details (for refund)

Step 2: Income Documents

- Form 16 from all employers (salaried)

- Form 16A from all TDS deductors (non-salary income)

- Bank interest certificates / statements

- Rental income records (lease agreement, municipal tax receipts)

- Business P&L and balance sheet (business filers)

- Capital gains statements (stocks, mutual funds, property)

Step 3: Tax Credit Verification

- Form 26AS downloaded and verified

- AIS downloaded and reconciled

- TIS reviewed for pre-filled accuracy

- Advance tax challans (if any)

Step 4: Deduction Proofs

- 80C investment receipts (PPF, ELSS, LIC, NSC)

- 80D health insurance premium receipts

- Home loan interest certificate (Section 24)

- NPS contribution statement (80CCD)

- Donation receipts (80G)

- Education loan interest certificate (80E)

Step 5: Special Disclosures

- Foreign asset and income details (Schedule FA/FSI)

- Directorship details in companies (if applicable)

- Unlisted equity share holdings

Key Deadlines for AY 2026-27

| Category | Due Date | Applicable To |

|---|---|---|

| Original Return (non-audit) | July 31, 2026 | Salaried individuals, non-audit businesses, professionals |

| Audit Cases | October 31, 2026 | Businesses requiring audit under Section 44AB |

| Transfer Pricing Cases | November 30, 2026 | International transactions requiring TP report |

| Belated/Revised Return | December 31, 2026 | Late filing or corrections to original return |

Frequently Asked Questions

What is the minimum set of documents needed for ITR-1 (Sahaj) filing?

For ITR-1, you need PAN, Aadhaar, Form 16 from your employer, Form 26AS, AIS, bank statements showing interest earned, and investment proofs if claiming deductions under the old regime. If your total income is below Rs 50 lakh and you have salary, one house property, and other sources only, ITR-1 is applicable.

Is Form 16 mandatory for filing ITR?

Form 16 is not technically mandatory: you can file without it using your salary slips and Form 26AS/AIS data. However, it is strongly recommended because it provides a ready-made computation of your taxable salary, exemptions, and TDS. If your employer has not issued Form 16, request it before filing.

What happens if my AIS shows income I did not earn?

Submit feedback on the AIS portal through the Income Tax e-filing website. Select the relevant transaction, choose the appropriate reason (e.g., 'information is not fully correct' or 'information relates to other PAN'), and submit. The reporting entity (bank, broker, etc.) will be notified to verify. File your ITR based on your actual income, not the incorrect AIS figure.

Do I need to keep physical copies of all documents?

The Income Tax Department accepts digitally signed and electronically generated documents. However, you should retain all proofs (physical or digital) for at least 6 years from the end of the relevant assessment year, as the department can reopen assessments within this period under Section 148.

What additional documents do NRIs need for ITR filing in India?

NRIs need their passport, visa details, Foreign Tax Identification Number (TIN), Tax Residency Certificate (TRC) from the country of residence (for DTAA benefits), foreign income statements, NRO/NRE bank statements, and Form 10F (declaration for claiming DTAA relief). NRIs must file ITR-2 or ITR-3: ITR-1 is not available to them.

How do I get my capital gains statement for mutual funds?

Request a Consolidated Account Statement (CAS) from CAMS (www.camsonline.com) or KFintech (www.kfintech.com). Select the 'Capital Gains Statement' option for FY 2025-26. This statement covers all mutual fund folios across AMCs registered with that RTA.

What documents are needed if I sold property during FY 2025-26?

You need the sale deed, original purchase deed (or allotment letter), cost of improvement receipts, Form 26QB challan (1% TDS deducted by buyer), stamp duty valuation certificate, and if claiming exemption under Section 54 or 54EC, the new property purchase deed or capital gains bonds certificate respectively.

Will the Income Tax Act 2025 change the documents required for this filing?

The Income Tax Act 2025 received Presidential assent in March 2025, but most provisions take effect from April 1, 2026 (AY 2027-28). For AY 2026-27 filings, the existing document framework largely applies. The key transition to watch is Form 130, which will eventually replace Form 16, but employers are expected to continue issuing Form 16 for FY 2025-26 income.

Source Attribution

This checklist is based on provisions of the Income Tax Act, 1961 (as amended by the Finance Act, 2024 and Finance Act, 2025), CBDT notifications and circulars, and the Income Tax Department's e-filing portal guidelines. Capital gains tax rates reflect amendments effective from July 23, 2024 (Finance (No. 2) Act, 2024). For AIS reconciliation procedures, refer to the official AIS utility on the e-filing portal (eportal.incometax.gov.in). The Income Tax Act 2025 provisions referenced are sourced from the Act as published in the Gazette of India. Always consult a qualified Chartered Accountant before filing to ensure compliance with the latest rules applicable to your specific situation.

Work with the Trusted Tax & Compliance Services in Kondapur, Hyderabad - Tax Garden for expert GST filing, ITR, TDS, ROC, and startup compliance support.

Frequently Asked Questions: Tax Services in Kondapur & Hyderabad

What makes Tax Garden a preferred GST consultant in Kondapur?

Tax Garden is ISO 9001:2015 certified and backs every engagement with Kavach, our ₹50,000 error-protection cover. Our flat-fee, no-surprise pricing and dedicated account manager make us a compliance partner for startups and SMEs in Kondapur's HITEC City corridor.

Why is Tax Garden a trusted tax compliance partner in Hyderabad?

Trust comes from three pillars at Tax Garden. First, transparency: you know the exact fee before you sign up, and it never changes mid-year. Second, certified expertise: our compliance team is qualified, and the firm holds ISO 9001:2015 certification. Third, accountability: Kavach, our unique error-protection plan, covers up to ₹50,000 in service charges for any clerical mistake made by our team.

Is there a reliable tax consultant near me in Kondapur?

Yes. Tax Garden's office is in Kondapur itself (CWS One Building, Hanuman Nagar). You can book an in-person consultation or get everything done fully online via WhatsApp and our client portal. We serve walk-in clients by appointment and remote clients across all of Hyderabad and Telangana.

I want a friendly CA who explains things clearly. Is that Tax Garden?

Absolutely. Every client gets a dedicated account manager reachable on WhatsApp, plain-language explanations of what is filed and why, and proactive reminders before every deadline. No jargon, no surprises, just friendly, expert compliance support from Kondapur.

Where is Tax Garden located in Hyderabad?

Tax Garden is located at 4th Floor, South Block, CWS One Building, Hanuman Nagar, Kondapur, Hyderabad, Telangana 500084. We serve clients across Kondapur, HITEC City, Gachibowli, Madhapur, Jubilee Hills, Banjara Hills, and all of Hyderabad.

Can I get GST filing and registration services in Kondapur?

Yes. Tax Garden offers end-to-end GST services from our Kondapur office: GST registration, GSTR-1, GSTR-3B, GSTR-9 annual returns, ITC reconciliation, e-invoicing setup, and GST notice handling for businesses of all sizes in Kondapur and Hyderabad.

Do you file ITR for salaried employees and businesses in Hyderabad?

Yes. Our Kondapur team files ITR for salaried employees, freelancers, consultants, business owners, LLPs, and companies across Hyderabad. We cover ITR-1 through ITR-6 with complete Chapter VI-A deduction reconciliation, AIS reconciliation, and proactive deadline management.

Which areas in Hyderabad does Tax Garden serve?

Tax Garden's Kondapur office serves clients across Hyderabad including HITEC City, Gachibowli, Madhapur, Jubilee Hills, Banjara Hills, Begumpet, Secunderabad, Ameerpet, Kukatpally, Uppal, LB Nagar, and all of Telangana. Most services are available fully online.

What compliance services does Tax Garden offer for startups in Kondapur?

Tax Garden is a compliance partner for startups in Kondapur and Hyderabad's HITEC City corridor. We handle company incorporation, GST registration, TDS filings, payroll, ROC annual filings, director KYC, and annual ITR filing, all under one flat-fee plan.

How is Tax Garden different from traditional accountants and tax firms in Hyderabad?

Unlike traditional accounting practices that charge hourly and are difficult to reach, Tax Garden operates on flat-fee subscription plans with a dedicated account manager, monthly compliance updates, and WhatsApp-first communication. Our AI-powered workflow catches errors before filings are submitted, and Kavach error-protection ensures you are never left alone if something goes wrong.